Pharmacy Benefits Research Unwrapped: Key Trends and Insights from 2024

Posted on December 10, 2024

Independent Pharmacy Benefit Research Helps Move the Industry Forward

For over 30 years, PSG has been a trusted independent voice in pharmacy benefits management. Our annual research series—comprised of four comprehensive reports—provides healthcare payers with critical insights into the evolving pharmacy benefits landscape. This year’s research captured impactful trends and highlighted the continued growth of the pharmacy market, with non-specialty and specialty drug spending growing at 12.8% and 14.0%, respectively. Through our rigorous independent analysis, we continue to drive market understanding and help stakeholders navigate complex pharmacy benefit challenges. In this annual review, we’ll highlight some of the most important findings from our 2024 research, offering an overview of critical trends, challenges, and opportunities in the pharmacy benefits space.

Traditional Drug Benefits

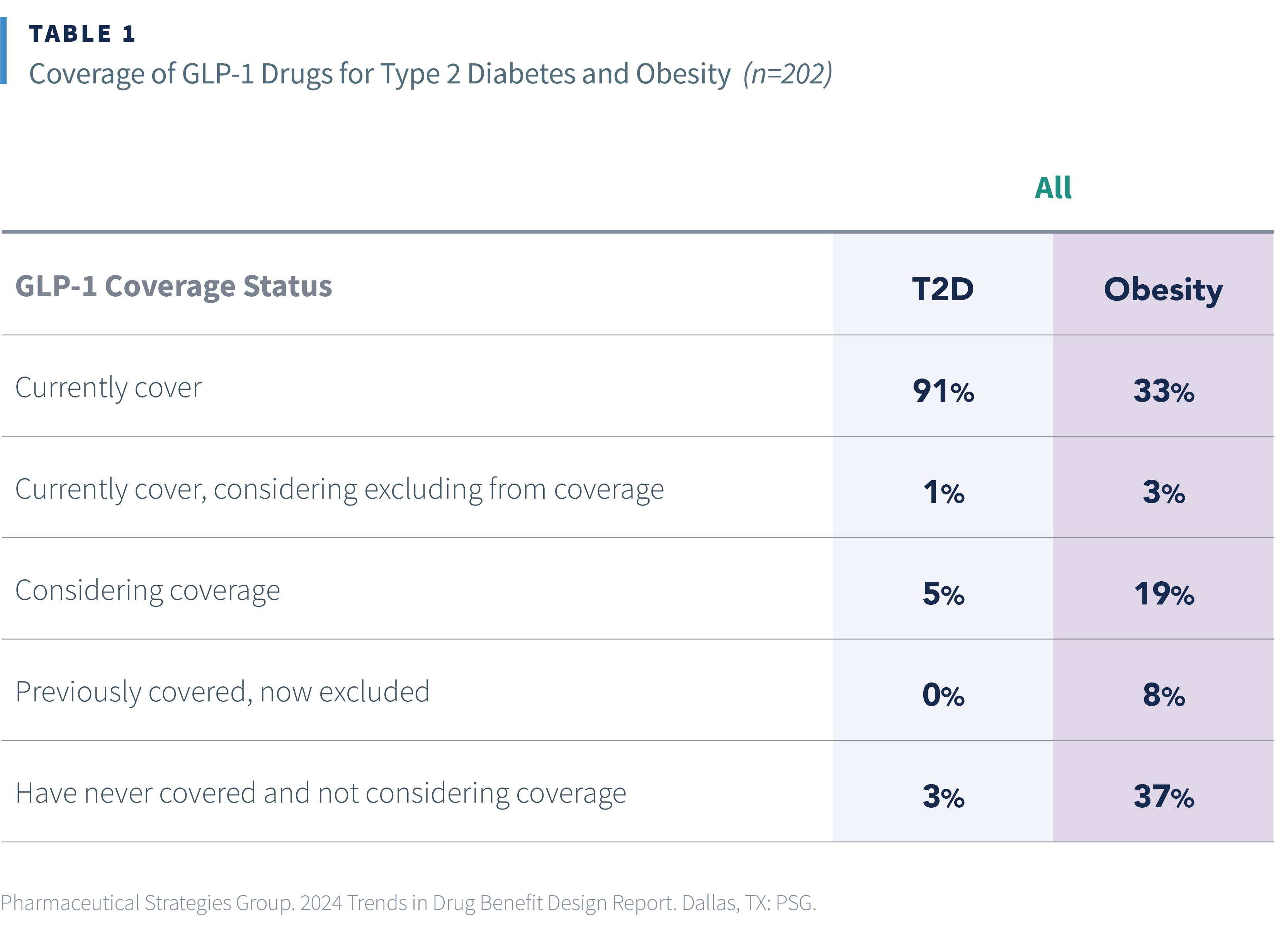

As anticipated, the GLP-1 medication class took the spotlight in non-specialty drugs this year. These drugs, first used to treat type 2 diabetes (T2D), have also shown effectiveness in treating obesity, and demand for GLP-1s has skyrocketed. However, the high cost of these medications has sparked debate about coverage options, particularly regarding weight loss and treatment of obesity.

Our research found that payers have mixed perceptions of obesity, with some viewing it as a lifestyle condition for which drugs should not be covered and others viewing it as a chronic condition appropriate for drug coverage. Consequently, when asked about their current GLP-1 coverage approach, only 36% of payers indicated that they currently cover GLP-1s for obesity, while 92% of payers cover GLP-1s for T2D. We also explored payers’ primary reasons for excluding GLP-1s for obesity from coverage. The main factor cited was the cost to cover all members for whom these drugs would be prescribed, followed by the belief that these are lifestyle drugs and thus not appropriate for coverage.

Beyond the pressing challenges of GLP-1 coverage, our analysis highlighted critical needs in health equity and transparency for members. Notably, only 1 in 5 payers reported having a process for tracking health disparities among their plan members, indicating a substantial opportunity for improvement in health equity initiatives. While this lack of insight into health disparities is concerning, there was broad consensus among payers regarding point-of-care benefit transparency – over 80% of respondents said it was moderately or very important to provide real-time cost and coverage information when members are making healthcare decisions. This alignment may suggest some industry recognition that empowering members with immediate access to benefit details can lead to more informed healthcare choices, improved medication adherence, and better overall health outcomes.

Specialty Drug Benefits

In the specialty drug domain, our research highlighted a tension between payers’ goals and areas of challenge. Managing total cost of care and controlling specialty drug spend emerged as payers’ most important priorities, yet persistent challenges in accessing reliable total cost of care data continue to undermine these efforts. This gap highlights the complexity of managing pharmacy benefits as well as the oft-mentioned challenge of transparency, leaving payers in a difficult situation when attempting to manage costs. Finding ways to better support members through lower costs was also a substantial challenge. Controlling costs while maintaining optimal clinical outcomes is an ongoing struggle payers must try to overcome.

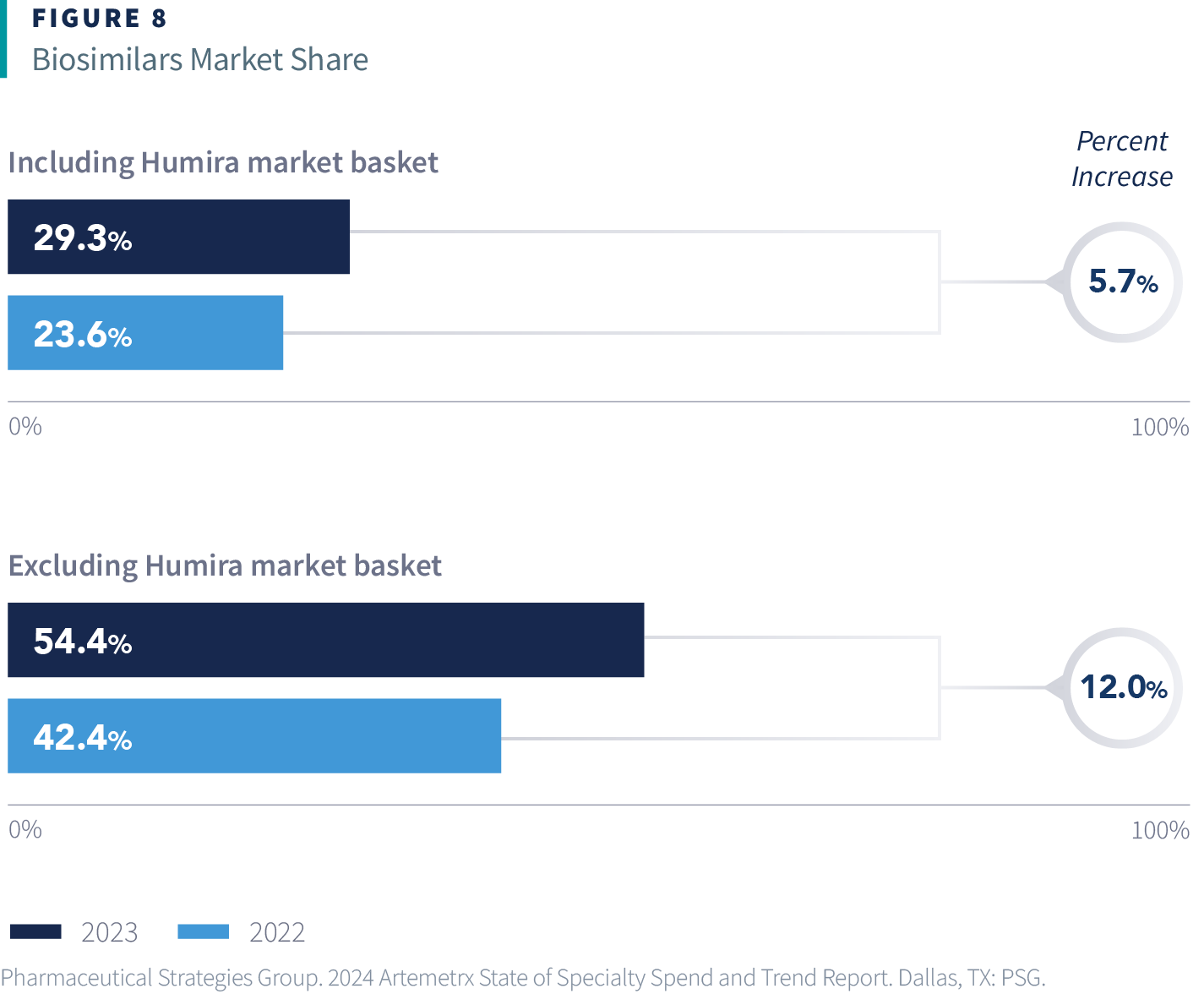

One area that could address both sides of this scale is maximizing the benefits of competition that biosimilars have brought to the market, which respondents also noted as a critical challenge. Although the biosimilar market as a whole is growing, its market share is heavily influenced by Humira, the top specialty drug by spend. In 2024, Humira continued to dominate the market, despite the recent introduction of its biosimilars.

Rebates can be a key driver of maintained brand use — payers are presented with an interesting decision between guaranteed rebate revenue from brand products or lower gross costs from biosimilars. The anticipated introduction of Stelara biosimilars in 2025 could further disrupt the market, potentially offering payers a meaningful pathway to cost mitigation.

Simultaneously, the cell and gene therapy (CGT) space has transitioned from a speculative future to an immediate strategic imperative. Projections indicate a staggering 3.5x increase in gene therapy spending over the next five years, creating a massive potential budget impact for healthcare payers. Our research found an interesting paradox: While the majority of respondents anticipate affordability challenges, a similar proportion report limited confidence in their understanding of the financial impact of CGTs. Additionally, only 11% of payers currently use financial protection products specific to CGTs, suggesting a potential preparedness gap.

As transformative specialty therapies continue to enter the market, payers face an urgent call to develop sophisticated financial strategies and a deep understanding of emerging treatments. The ability to navigate this complex landscape will likely determine which organizations can successfully balance innovation, patient care, and fiscal sustainability.

Industry Transformation and Change

In addition to the key themes mentioned above, the pharmacy benefit manager (PBM) industry is experiencing notable change. Our research found that declining customer satisfaction, rising costs, and increased scrutiny of PBM practices are driving desire for innovation. Transparency has emerged as a central theme, with our findings identifying multifaceted concerns from payers. Many payers perceive their current PBMs lack transparency regarding rebates and sources of revenue, and approximately two-thirds are actively seeking more transparency and accountability for costs and outcomes in their utilization management programs. Compounded by the persistent challenges in accessing total cost of care data mentioned earlier, one can see why PBM transparency has become a focal point of healthcare payers.

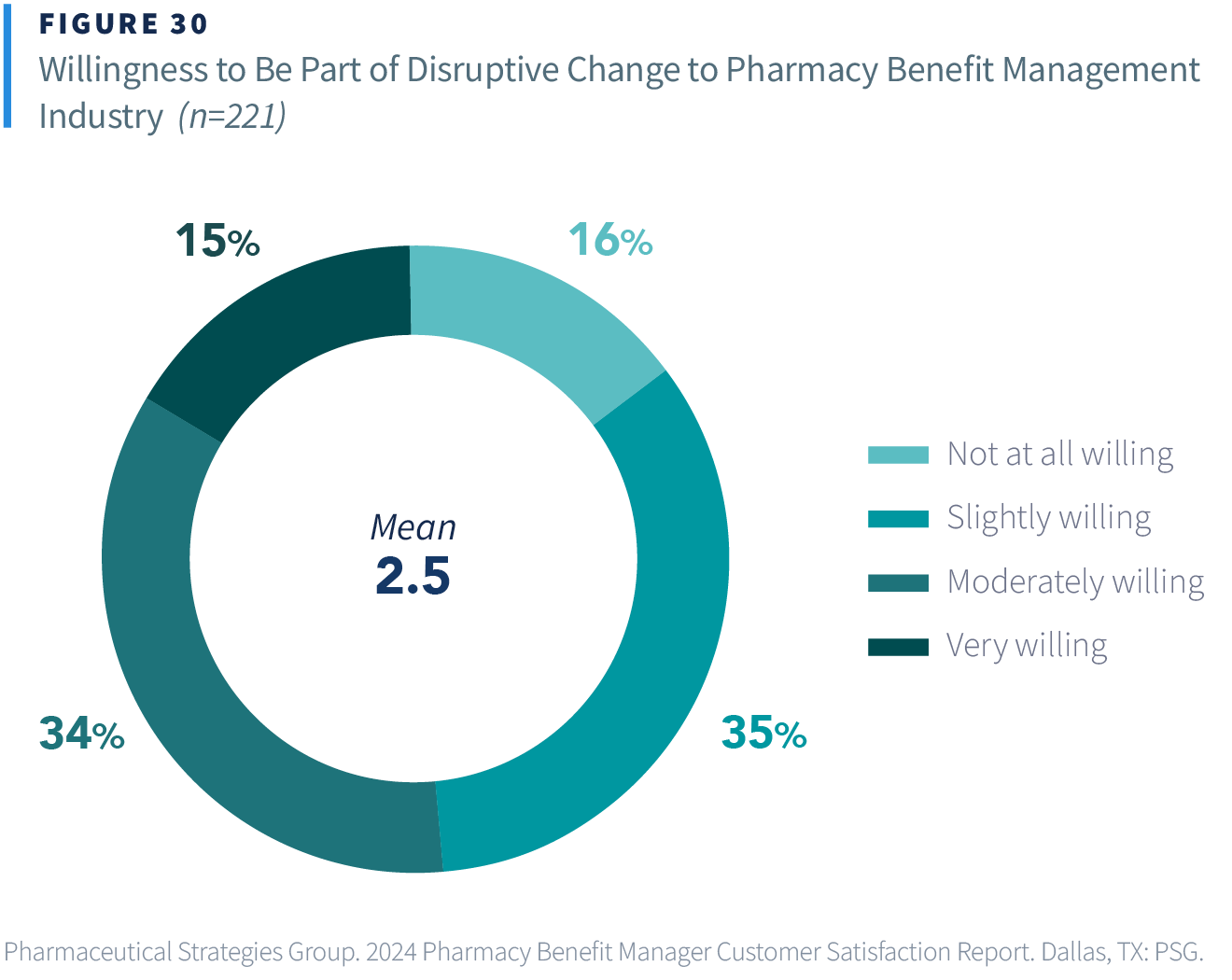

Our research revealed a strong desire for change in the PBM industry for over 50% of payers. However, a desire for change does not always equate to willingness and ability to drive change. Payers were nearly evenly split between being not at all or somewhat willing or moderately or very willing to be part of disruptive change at this time. Payers who are ready to be part of disruptive change have a variety of avenues available to them including adopting alternative pharmacy pricing models, using a mid-market or emerging PBM, carving out some PBM services, fully unbundling the PBM, and more.

Advancing Pharmacy Benefits Research, in 2024 and Onward

As we reflect on the year’s research, our insights underscore the dynamic and complex nature of pharmacy benefits. Our comprehensive reports have become a cornerstone of market intelligence, reaching thousands of individuals and capturing the perspectives of healthcare leaders throughout the industry.

We recognize the power of our research lies in collaborative engagement—whether through the voices of the industry professionals who share their insights or the forward-thinking organizations that support our mission. By participating in our annual surveys or sponsoring our market-defining reports, you become an integral part of advancing pharmacy benefit understanding.

Take the next step in helping to shape the future of pharmacy benefit research. Your participation—whether through insights or report sponsorship —drives the research that transforms our industry.