Medicare Publishes Results of the Drug Price Negotiation Program

Posted on August 23, 2024

Plans must evaluate the adverse impact of the published Drug Price Negotiation Program

On August 15, 2024, the Centers for Medicare and Medicaid Services (CMS) announced the first round of negotiated prices for 10 drugs. CMS is stating that these prices represent a 22% savings or roughly $6B in reduced Part D spend if the program were in place in 2023. To get to this point:

- CMS held three meetings with each participating drug company to discuss the offers and counteroffers and attempt to arrive at what officials said was a “mutually acceptable price” for the drug.

- Negotiated prices were reached for five of the drugs during those meetings. Administration officials accepted manufacturer counteroffers for four of those drugs.

- For the other five, CMS issued a final written offer to the pharmaceutical companies, which was later accepted.

Negotiation Outcome – Was it the Maximum? Was it Fair?

The following table lists the 2026 Selected Drugs and their Maximum Fair Prices (MFPs).

| 2026 Selected Drugs | 2024 Average Wholesale Price (AWP)/NDC Unit | 2026 Maximum Fair Price (MFP)/NDC Unit | Unit Cost Reduction (2024 AWP vs. 2026 MFP) |

|---|---|---|---|

| Januvia | $22.92 | $3.91 | -79% |

| Novolog | $8.68 | $8.96 | 3% |

| Fiasp | $42.99 | $8.96 | -75% |

| Farxiga | $23.29 | $6.05 | -68% |

| Enbrel* | $2,220.55 | $583.54 | -68% |

| Jardiance | $24.44 | $6.79 | -66% |

| Stelara* | $33,411.42 | $8,979.65 | -67% |

| Xarelto | $22.78 | $6.88 | -63% |

| Eliquis | $11.89 | $4.15 | -57% |

| Entresto | $13.76 | $5.23 | -54% |

| Imbruvica* | $702.49 | $353.94 | -39% |

On the surface, the MFPs for 2026 seem like steep discounts to current AWP prices, except for Novolog, which already experienced a decrease in price effective January 1, 2024. CMS was able to drive significantly below the ceiling price, or highest price CMS can accept by law, for all but three of the ten drugs. Remaining patent life and availability of lower-cost therapeutic alternatives were common characteristics among the drugs with deepest discounts. Imbruvica is the drug driving the highest net benefit since there are little to no rebates available for the product today.

There still is a question of whether this process is more effective than the current process or simply creates a less conflicted process. PBMs have been undergoing an inquiry by the FTC. Last month, Congress questioned for-profit PBMs and how they negotiate with for-profit pharmaceutical manufacturers and earn revenue from those efforts.

The fairness of the negotiated prices and process remains up for debate. The 2026 Selected Drugs set a precedent and provide insights into how CMS may handle future negotiations. The reaction from Wall Street and the narrative from several Pharmaceutical Manufacturer executives on earnings calls has been positive in the sense that the outcome was favorable or “could have been worse.” However, there still are concerns from manufacturers on the process and evaluation of comparing the pricing of therapeutic alternatives and the ultimate penalty of being excluded from Medicare Part D and Medicaid.

Who is Saving? And How Much?

To independently assess CMS’ savings figures, we evaluated 2022 Medicare Part D utilization data within our book of business to current 2024 pricing (including rebate estimates) and current and future Part D design. The findings are as follows:

| 2024 AWP | $61,730,832,255 | 2022 Part D utilization applied against July 2024 AWP in MediSpan |

| 2024 Drug Spend | $50,619,282,449 | AWP-18% discount |

| 2024 Estimated % Rebates (% of Spend) | 47% | Estimated rebates (weighted) |

| 2024 Estimated Rebate Dollars | $23,598,516,113 | 2024 Drug Spend * % Estimated Rebate |

| 2024 Net Price | $27,103,461,483 | 2024 Drug Spend minus Estimated Rebate $ |

| 2024 Net Plan Liability | $4,233,800,082 | Applies 2024 Drug Spend and Rebates to 2024 Part D design (40% of Drug Spend and 68% of Rebates are retained by plan) |

| 2025 Part D Redesign Net Plan Liability | $10,126,462,700 | Applies 2024 Spend and Rebates to 2025 Part D Redesign (60% of Drug Spend and 86% of Rebates are retained by plan) |

| 2026 Drug Spend | $19,935,591,946 | Assumes 2022 Part D utilization against August 2024 published Maximum Fair Price |

| MFP Effective Discount (vs. 2024 Drug Spend) | 61% | 2024 Spend minus 2026 Spend/2024 Spend |

| 2026 Plan Liability | $11,961,355,168 | Assumes plan is liable for 60% of 2026 Drug Spend |

Our calculated average discount for the Maximum Fair Price of 2026 Selected Drugs represents roughly a 61% decrease in costs at point of sale. If our rebate assumptions are accurate, this would result in a financial detriment to Part D payers compared to the 2025 net economics with rebates. The “break-even” point (2025 with rebates vs. 2026 at MFP) is variable between payers, depending on the mix of Selected Drugs. For example, a plan that is receiving rebates on Selected Drugs that reflect about 46% of Wholesale Acquisition Cost would need to see a 65% reduction in Ingredient Cost. In other words, health plans are about the same or slightly worse off financially than when PBMs and rebates were the levers used to negotiate lower prices for these ten drugs.

Another question is how MFP compares to what other countries pay for these drugs. The Office of the Assistant Secretary for Planning and Evaluation (ASPE) released a study in February 2024 that estimated that brand drug prices (net of rebates) in the US are 322% of the prices paid by other countries (e.g., UK, Canada, France, Germany, Japan). Medicare Drug Price Negotiation and MFP help to close some of the gap between the U.S. and other countries, but a significant delta remains.

Our analysis shows a ~$7B ($27.1B in 2024 vs. $19.9B in 2026) difference in 2024 drug spend net of rebates in comparison to 2026 Drug Spend based on MFP before applying factors for member cost-sharing, Manufacturer Gap Discount, CMS reinsurance, or other subsidies. We did not assume any increases in utilization of Selected Drugs from 2022. This is our best assumption on how CMS derived its $6B savings (22% savings).

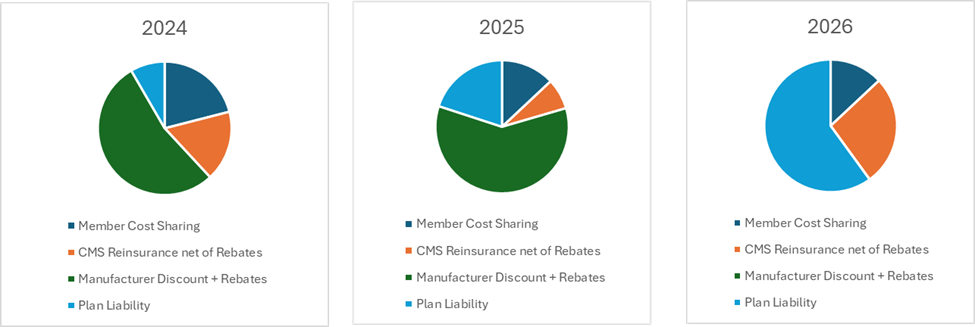

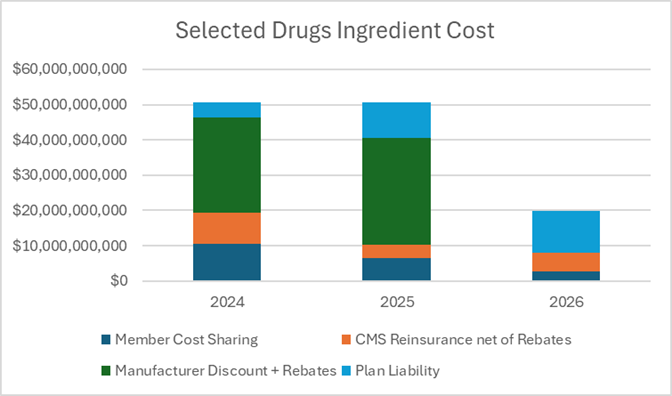

Who is Paying for Selected Drugs?

The Inflation Reduction Act (IRA) is changing more than just the price of drugs. Simultaneously, we are undergoing a transformation with a shift in liability between the four parties that pay for Part D drugs (members, manufacturers, CMS, and plans). Members are seeing most of the benefit from the IRA overall, as intended. Members are paying a lower portion of drug costs for Selected Drugs compared to today and, overall, are paying less as the ingredient cost of Selected Drugs decreases.

Health Plans are paying a substantially larger portion of ingredient costs for Selected Drugs, going from a net plan liability of $4B in 2024 to almost $12B in 2026.

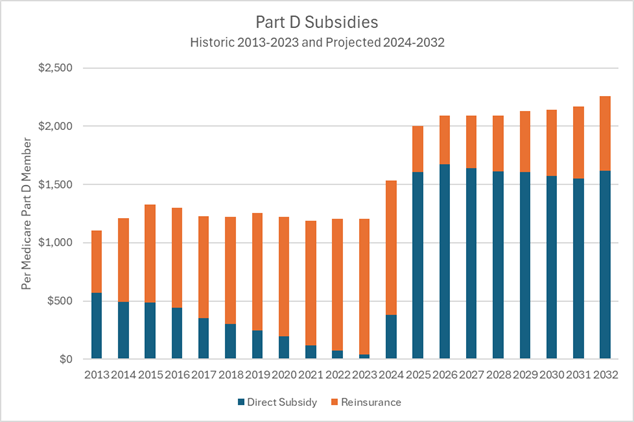

CMS is also seeing decreases in reinsurance, but that does not directly correlate to savings for the federal government. Direct Subsidy, which is made prospectively and based on Risk Adjustment, is projected to increase significantly by CMS in 2025 and the coming years. The table below shows CMS’ projected per member subsidy for all Part D members.

Now that the MFPs have been published, plans must evaluate the strategic and operational impacts in advance of the 2026 bid submission deadline in June 2025. PSG has a highly experienced team of experts that can assist with navigating these changes, including Part D plan design and formulary management. Please contact us if you’d like to learn more.