Real Questions, Real Answers: Understanding the adoption and pipeline for biosimilars

Posted on November 13, 2020

Join the discussion already in progress as we shift gears from last week’s installment on “Unpacking utilization and medical pharmacy integration” to this week’s segment on biosimilars.

Part Two: Biosimilars – Understanding adoption and pipeline

Q: Let’s shift the focus to another popular topic: biosimilars. Renee, will you share insights on where and how we realize the promise of biosimilars? Are they starting to drive material savings?

Renee Rayburg:

Sure. We have been waiting for a while. The United States was behind some other countries in the development of a pathway for approval of biosimilar drugs. It’s exciting now to see that we are making great strides here. In the U.S., the FDA has approved 28 biosimilars to date, ten of which were approved in 2019.

While not all of them are currently available because in some cases, where there are several biosimilars for drugs like HumiraⓇ and EnbrelⓇ, there have been legal processes that have come to agreements with those companies to delay the biosimilar launch. But there are others on the market, and we’ve started to see some uptake.

What’s interesting is the effect of the presence of biosimilars in the market has had. We expect them to enter the market at a lower price, which they have, but their brand name counterparts are still around, and for some drugs, this has led to a decrease in unit cost for all drugs.

What may achieve the most significant savings may not necessarily be the biosimilars themselves. Instead, it’s the biosimilars’ presence and the competition they are creating in the market.

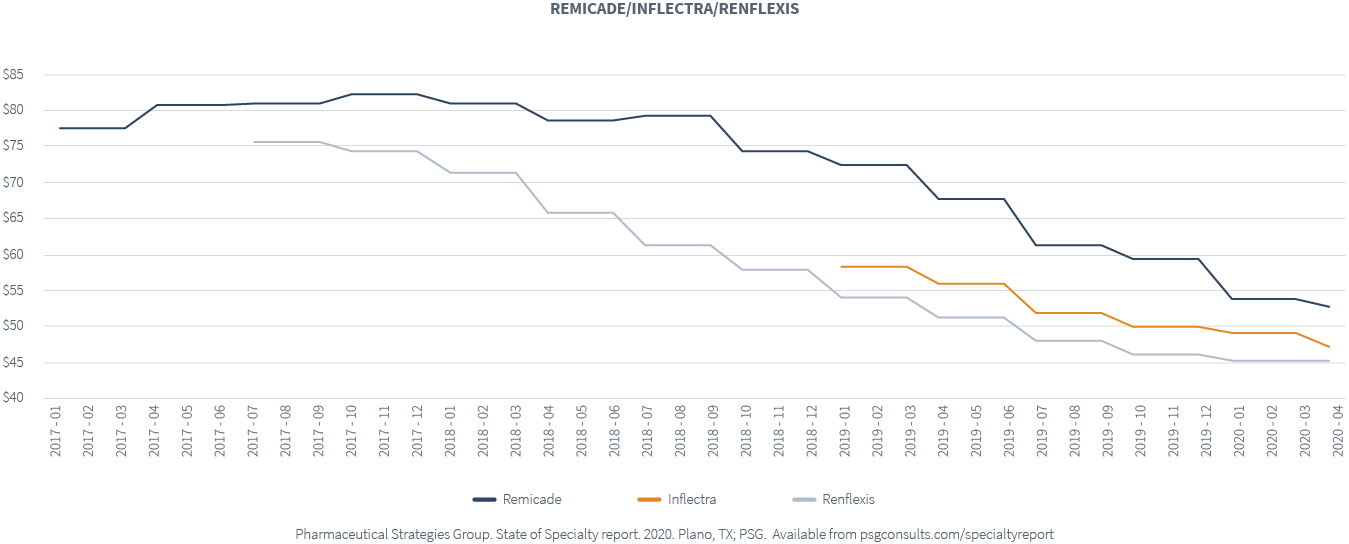

The shift to biosimilars is slow for some chronic conditions. For example, think about RemicadeⓇ. There are four approved biosimilars, while only two are available, InflectraⓇ and RenflexisⓇ.

We haven’t seen a strong uptake in the biosimilars themselves. Where there is biosimilar usage, costs are decreasing. Nonetheless, we have also seen the price of Remicade decrease too. As these two biosimilars hit the market, the cost of Remicade decreased by about 20 percent across our book of business.

Biosimilars have generated a lot of interest, but we need to continue approaching drug management strategically. Don’t lose sight of which product offers you the lowest net cost because it may not be the biosimilar. Surprisingly, it might be the brand name drug. Either way, we believe that the competition biosimilars are bringing to the market will lead to cost savings.

Q: What about biosimilars and oncology drugs? What is happening with biosimilars in that category?

Renee Rayburg:

We see an uptick in biosimilars for some of the oncology drugs. Many health plans exclude coverage of the branded drugs, AvastinⓇ and HerceptinⓇ, and are covering their biosimilars instead. This is a biosimilar strategy that seems to be becoming more popular.

Then we have biosimilars like NeulastaⓇ , a drug with four biosimilars that have been approved in the U.S. market. And, yet, we haven’t seen a substantial uptake. Part of that is because the brand product has a unique dosage form. The on-body OnproⓇ allows the patients to get their chemotherapy and then administer their Neulasta at home themselves the next day. They attach a device to the patient’s arm, which can deliver the drug the next day instead of having to return to the physician’s office. That can make a difference for some patients. None of the biosimilars have that unique dosage form, which may be why we do not see a strong uptake.

I will add that I’ve seen some of the upcoming PBM formulary changes, and they’re starting not to cover the brand Neulasta and cover the biosimilars instead. We also saw an increase in UdenycaⓇ, one of the biosimilars, across our book of business in 2020.

It’s exciting, and there’s more to come. But understand where the savings are originating, and then make sure that you optimize and use the product that will bring you the lowest net cost.

Q: This will be a topic we’ll be watching for years to come. So, in a similar spirit, let’s talk about the pipeline. In 2019, 48 new drugs were approved, 29 of which were specialty drugs. It’s not surprising that specialty drugs are dominating the market and innovation. What are you expecting with the specialty drugs that are in the pipeline?

Renee Rayburg:

Science is advancing. The pipeline continues to be robust. I suspect that is contributing to the increases in trends that we talked about earlier. But even for this year, in 2020 through September, we’ve had 40 new, FDA-approved drugs. About half of them are specialty drugs.

- In that mix, we’ve seen the approval of one new gene therapy, Tecartus™. It is a CAR-T cell therapy approved in July to treat mantle cell lymphoma with a price tag of $373,000. The price is in line with the other CAR-T cell therapies, but it’s adding to that mix. Then we have some notable approvals still waiting and pending review for this last quarter of 2020.

- There could be another CAR-T cell therapy, Liso-cel, for non-Hodgkin’s lymphoma. It’s a Bristol Myers Squibb drug looking to be reviewed in mid-November.

- There is also RoxadustatⓇ, an oral dosage drug used for anemia and anemia of chronic kidney disease. Today, those patients with chronic kidney disease require anemia drugs, which are injections. There are a couple of different oral medications in the pipeline, and this one seems to be the front runner. We expect its review in December.

It’s always promising and exciting when science advances, but it is essential to do the right things to ensure the affordability and availability of these therapies for patients who need and can benefit from them.

Q: We love to hear about these promising drugs that could be coming to market soon, but what about the ones we have been planning for that failed to achieve FDA approval?

Renee Rayburg:

There have been some denials, especially over the past summer. So, you don’t see or hear a lot about the denials, but four different specialty drugs did not get FDA approved this past summer. They all received a complete response letter in which the FDA lays out what they need from the products in order to re-submit.

Let’s focus on the hemophilia A gene therapy for a moment. We had been preparing clients for a while about this drug. Everyone was trying to understand how it was going to fit into the treatment paradigm. Many of these other gene therapies that come to the market are for patients who have exhausted all treatments. Gene therapies are often the last resort, especially CAR-T cell therapies.

This one was different as there are many drug therapies available for hemophilia A patients. The gene therapy offered the hope of better quality of life by eliminating the need for ongoing prophylactic therapy, often administered multiple times a week, and eliminating or decreasing bleeds. There was a lot of excitement in the hemophilia community, but it didn’t get approved. The FDA was concerned about the durability of the drug. It showed that it did work as it decreased 96 percent of bleeds for hemophilia A patients, but the drug itself started to wane over time. After a three or four-year period, they began to see decreases and questioned if the positive effects of the drug were sustainable over time. That was concerning because gene therapies are one-time therapies.

The FDA has asked them to complete their phase three study and do a two-year follow-up. They will have an opportunity to continue to study the drug. I think for the moment, it is not going to be on anyone’s radar. The earliest it may be reviewed is mid to late 2022. The cost is concerning. The estimated price tag for that drug was between $2 and $3 million. For now, we’ll continue to monitor it, but those patients will remain on available therapies, and we’ll see where that goes.

I think it’s very telling and, in some ways, good that the FDA is evaluating some of these concerns in their process. Payers were undoubtedly concerned about how to afford a $2 or $3 million drug, even without many hemophilia members.

There’s pressure now being put on these companies, especially those delivering the gene therapies they must provide a solid value proposition.

It hearkens back to this opportunity and the need to look at the total cost of care. Historically any of the specialty medications requiring investments at that level in your health plan members, your employees, and the ability to see what the outcomes look like for those medications is so critical.

Stay tuned for the next part in this series, Utilization Management: How to achieve best practices in the managed care space, launching in the new year.

If you don’t want to wait until next week for more information, download the 2020 State of Specialty Spend and Trend Report today!